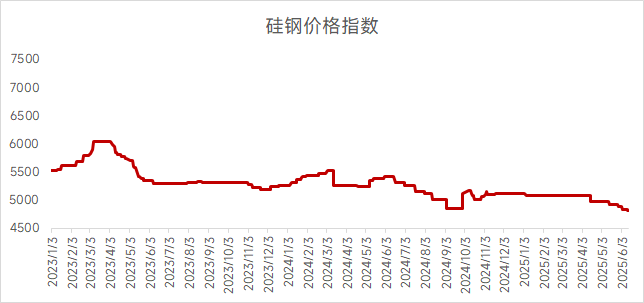

Non-Oriented Electrical Steel Price Dynamics

Shanghai B50A800 grade: 4,900-4,950 yuan/mt

Wuhan 50WW800 grade: 4,650-4,750 yuan/mt

Guangzhou B50A800 grade: 4,550-4,650 yuan/mt

Shanghai market:

This week, cold-rolled non-oriented electrical steel prices in Shanghai dropped slightly, with overall market transactions in the doldrums. The ferrous metals series futures market fluctuated, while HRC spot price movements were relatively small. However, long-term expectations for finished product prices remained downward, continuing to negatively impact the non-oriented electrical steel market. On the supply-demand front, non-oriented electrical steel supply remained ample, particularly from private mills facing intense sales competition and weak price support. State-owned enterprise resources faced relatively small supply pressure, with overall inventory at low levels, keeping prices firm. Additionally, the market was in the off-season, with narrowing order growth from downstream automotive and home appliance industries, limiting demand increments. Looking ahead, non-oriented electrical steel supply tightened as some mills voluntarily cut production, improving the oversupply situation. However, insufficient demand release and modest order growth from downstream end-users kept market participants cautious. Shanghai non-oriented electrical steel prices are expected to retain some downside room next week.

Wuhan market:

This week, cold-rolled non-oriented electrical steel spot prices in Wuhan held steady, with weak transaction performance. The ferrous metals series futures market fluctuated, but weak market confidence kept trading sentiment below average. Fundamentally, delayed supply increments from state-owned enterprises kept medium and low-grade spot resources scarce. However, traditional off-season demand weakened downstream end-user purchase willingness, with traders ordering cautiously. Most market participants held bearish expectations, maintaining low inventory levels without restocking motivation. Few inquiries were recorded. Going forward, the off-season effect persists with low transaction activity, though state-owned enterprises show strong reluctance to budge on prices. Wuhan non-oriented electrical steel prices may undergo narrow-range adjustments next week.

Guangzhou market:

This week, cold-rolled non-oriented electrical steel prices in Guangzhou dropped slightly, with lackluster spot market trading activity. Ferrous futures showed volatile trends, while decent HRC spot margins led to widespread expectations of cost downside, weakening price support. Fundamentally, scarce tradeable resources and low trader inventories coincided with intensifying off-season impacts. Downstream terminal production remained moderate, with cautious purchasing and low inventory-building willingness sustaining weak transactions. Subsequently, worsening off-season effects created dual weakness in supply and demand within the trade sector. Given generally ample supply, Guangzhou non-oriented electrical steel prices are expected to remain in the doldrums next week with some downward potential.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)